Right to Repair: Deere Lawsuit Reshapes Parts Market

title: "Right to Repair: The Shifting Parts Market Behind John Deere's Lawsuits"

date: 2026-07-17

author: EquipNode

category: Parts Aftermarket

tags: [Right to Repair, Parts Market, John Deere, Aftermarket, Construction Machinery Maintenance]

In July 2026, U.S. federal courts once again took up a right-to-repair lawsuit against John Deere. This isn't the first time Deere has found itself in the defendant's chair — from agricultural equipment to construction machinery, the Right to Repair movement is fundamentally reshaping the entire industry's parts supply chain and aftermarket landscape.

The Right-to-Repair Storm: From Farm Equipment to Construction Machinery

At the end of 2025, John Deere reached a $99 million settlement in the agricultural equipment sector, allowing farmers to repair their own equipment. But Wyoming ranchers argue the amount is far from sufficient. In early 2026, advocacy organizations turned their sights on Deere's construction machinery product lines.

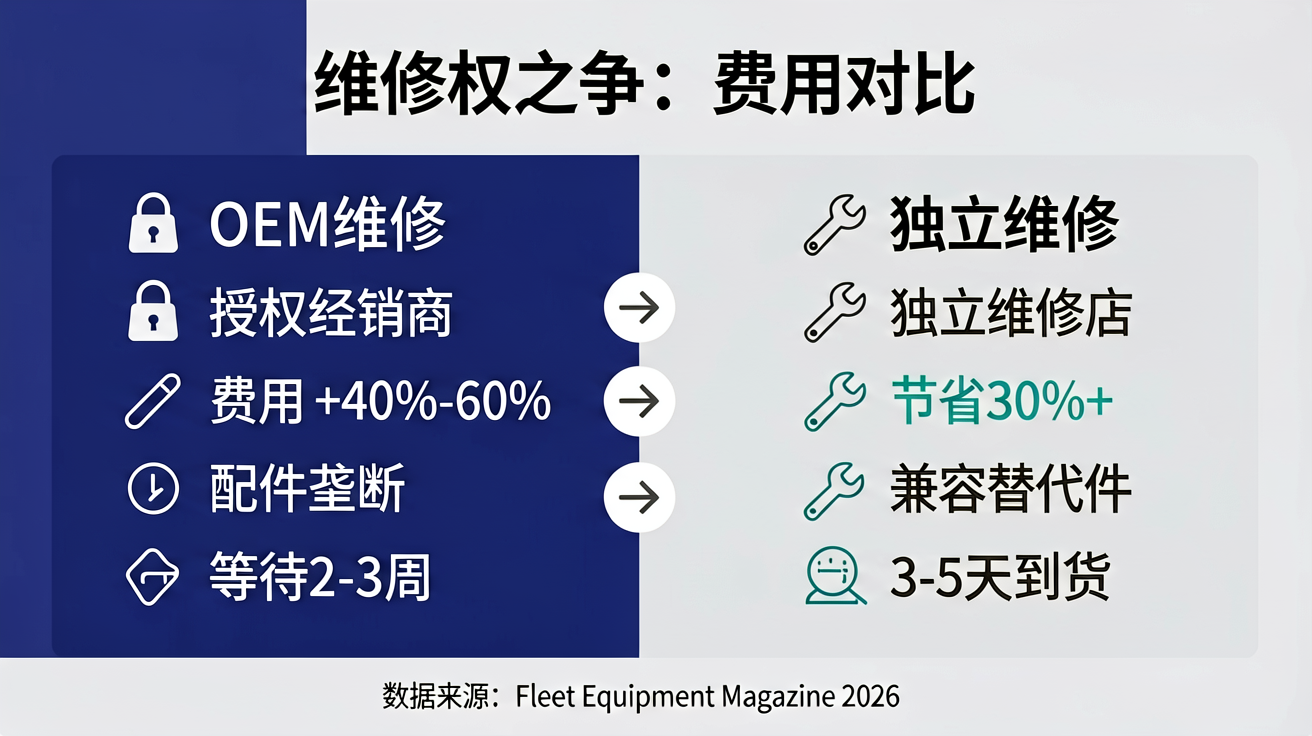

The core dispute: through encrypted electronic control systems and proprietary diagnostic software, Deere has effectively monopolized the repair market. Equipment owners purchase their machines but cannot independently replace sensors, calibrate hydraulic systems, or even read fault codes. A WSJ report highlights that this "repair lock-in" model forces users to rely exclusively on authorized dealers, with repair costs running 40%–60% higher than those at independent shops.

For Chinese brands such as SANY and XCMG, this represents both a challenge and an opportunity. In the global construction machinery aftermarket, whoever can offer a more open parts supply and more flexible repair solutions will earn greater customer loyalty.

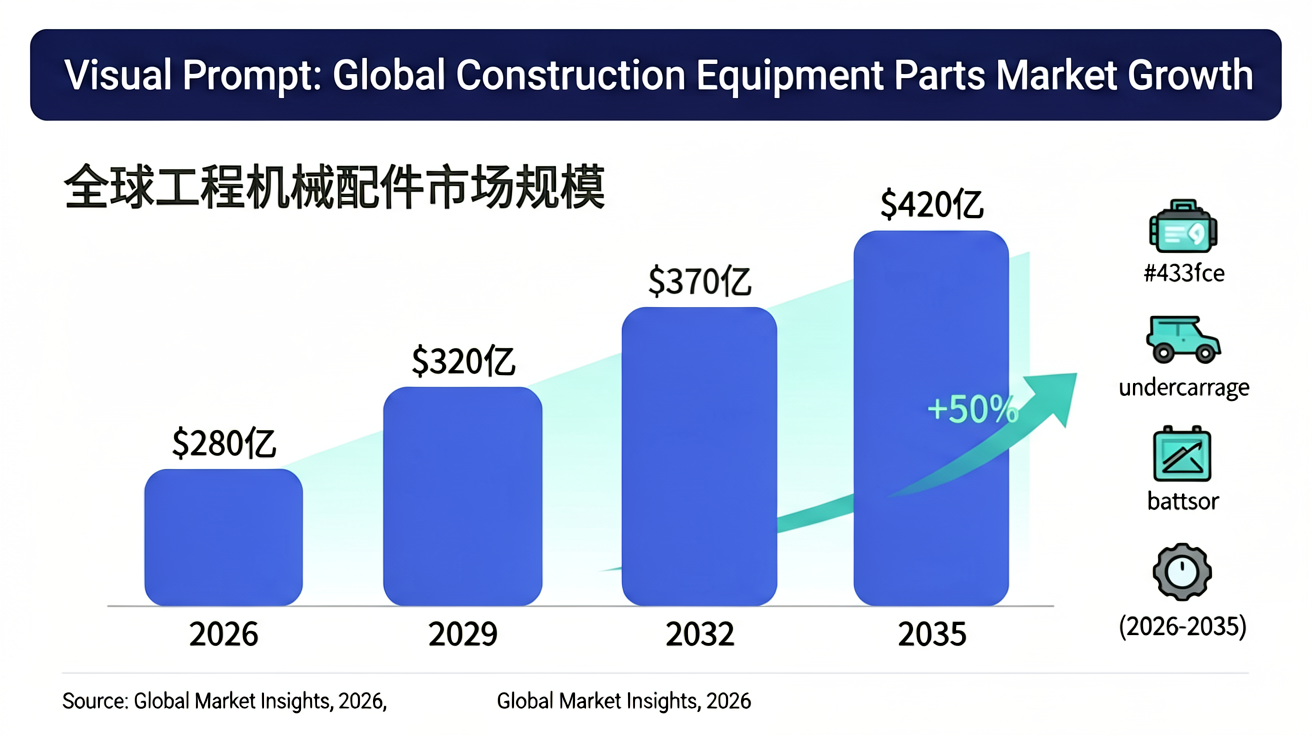

The Parts Market: A $28 Billion Pie Being Repportioned

The latest report from Global Market Insights shows that the global construction machinery engine services market reached approximately $28 billion in 2026, with projections of growth beyond $42 billion by 2035.

Key drivers of this growth include:

- Continuously expanding equipment fleet: The global construction machinery fleet has surpassed 20 million units, with average machine age rising to 8–12 years, pushing maintenance demand into a peak cycle

- Electrification creating new parts demand: Surging need for battery management systems, electric motor controllers, energy recovery systems, and other new components

- Widespread adoption of predictive maintenance: IoT sensors and AI diagnostics are making "on-demand repair" possible, while simultaneously increasing demand for specialized parts

IndexBox data indicates that the heavy-equipment undercarriage parts market is also growing rapidly. Annual replacement market value for track pads, carrier rollers, and idlers alone has exceeded $6 billion.

SANY's Aftermarket Strategy: From Selling Equipment to Selling Services

At the ConExpo-Con/AGG show in March 2026, SANY America announced a series of new aftermarket service initiatives, showcasing Chinese brands' strategic transformation in the parts space:

E-commerce parts platform launch: Customers can now order OEM parts directly through an online platform, with delivery cycles reduced from the traditional 2–3 weeks to 3–5 days

Cross-reference database opened: Third-party suppliers such as Fab Heavy Parts leverage OEM cross-reference data to help users find compatible aftermarket alternatives, reducing repair costs by more than 30%

Mobile repair service stations: 50 mobile service stations deployed across North America, covering major construction machinery concentration areas

This "equipment + service + parts" lifecycle model is emerging as a key differentiator for Chinese construction machinery brands going global.

The Survival Playbook for Independent Repair Shops

Facing OEM technical lockdowns and pressure from dealer networks, independent repair shops are carving out new survival space:

On the technical front: Open diagnostic tools — such as open diagnostic protocols — are enabling users and independent technicians to access equipment data. Right-to-Repair legislation is advancing in multiple states, requiring manufacturers to provide repair manuals and diagnostic interfaces.

On the parts front: The third-party parts market is becoming more standardized. ISO-certified aftermarket components now rival OEM parts in quality, typically priced at 50%–70% of OEM cost. The critical factor is building a reliable quality traceability system.

On the service front: Predictive Maintenance is shifting repair from "fix it when it breaks" to "replace before failure." By monitoring hydraulic oil quality, filter differential pressure, and vibration frequency through IoT sensors, components can be precisely replaced before faults occur, reducing unplanned downtime by over 60%.

Practical Tips for Parts Purchasing

For equipment owners and maintenance managers, the following points are worth considering:

Distinguish between safety-critical and consumable parts: Use OEM parts for safety-critical components such as braking systems and crane booms; ISO-certified alternatives are suitable for consumables like filters and bucket teeth

Track parts shelf life: Hydraulic seals and rubber hoses have defined shelf lives (typically 3–5 years), and using them beyond expiry carries significant risk

Maintain a parts inventory ledger: Use equipment operating hours to forecast replacement cycles and pre-order parts to avoid costly downtime

Leverage digital tools: Use equipment management apps to track parts replacement history, inventory status, and supplier quotes

For specific equipment parts pricing and supply information, feel free to contact our sales team for a tailored solution.

Industry Outlook

The deepening Right to Repair movement will drive the construction machinery aftermarket toward greater openness and transparency. For Chinese construction machinery brands, this is both a window of opportunity to enhance global competitiveness and a critical juncture for transforming from "equipment manufacturers" into "full-lifecycle service providers."

Over the next 3–5 years, we expect to see: OEM parts pricing power gradually eroded, third-party certification systems becoming more established, predictive maintenance becoming standard, and parts e-commerce penetration rising sharply. Whoever moves fastest on these trends will gain the upper hand in this $28-billion aftermarket race.